Companies as Part of Civil Society

Abstract [en]: As societal expectations towards company values increased over time, there is an ongoing discussion about the role of companies in civil society. Therefore, this paper briefly defines basic concepts like values, ethics and civil society and analyzes Merck’s actions, their code of conduct and corporate responsibility report. Conducting a small-scale ethical evaluation rating according to Ulrich Hemel (2019) as well as an investigation of corporate codes in accordance with Muel Kaptein (2004), leads to conclusions whether Merck consider themselves to be agents in civil society. My analysis indicates that Merck is well aware of their ethical and social affiliation to civil society. For instance, they clearly define their corporate values in a detailed manner, while at the same time pursuing activities that enable a matching corporate culture.

Abstract [de]: Mit dem Anstieg der gesellschaftlichen Erwartungen an Unternehmenswerte im Laufe der Zeit haben sich auch Diskussionen bezüglich der Rolle von Unternehmen in dem gesamtgesellschaftlichen Zusammenhang ergeben. Dieser Beitrag untersucht daher beispielhaft Merck‘s Unternehmungen, Unternehmenskodex sowie den Bericht zur Unternehmensverantwortung und definiert hierfür die notwendigen Terminologien der Werte, Ethik und Zivilgesellschaft. Die Durchführung einer Wahrnehmungsstudie von Partizipierende eines Universitätskurses nach Ulrich Hemel (2019), sowie eine Untersuchung des Unternehmenskodex von Merck, in Anlehnung an Muel Kaptein (2004), sollen hierbei zu einer abschließenden Beurteilung darüber führen, ob sich Merck als Teil der Zivilgesellschaft zu betrachten scheint. Meine Analyse führt zu dem Ergebnis, dass sich Merck der gesellschaftlichen Rolle bewusst ist. So definiert Merck unter Anderem ausführlich die eigenen Unternehmenswerte und führt Maßnahmen zur Einhaltung und Implementierung dieser auf.

April 2020

Companies as Part of Civil Society

An exemplary evaluation of Merck KGaA

1 Introduction

For decades there has been theoretical progress in the perception of company values and company responsibility. While Milton Friedman found the shareholder value principle to be the leading factor of corporations back in the 1970s (Friedman, 1970), it was in the 1990s, that Carroll et al. (1991) shaped this view towards a more socially engaged perspective of corporations. In the 2000s and 2010s, Freeman (2001) as well as Porter and Kramer (2011) then intensified this view even more towards stakeholder and shared value. Historically, it can therefore be noticed, that economists developed companies’ purposes from sole profit maximization towards attributing value to various stakeholders of civil society.

This theoretical progressive desirability can also be underlined by concrete practical actions, like the augmented formulation of social goals and norms. Among others, the development of the Sustainable Development Goals (SDGs), with its introduction in 2014 by the United Nations (UN), can be seen as one of those indicators of an increased perception of desired sustainability of companies in practice (Sachs, 2012). It elucidates that the interest in companies’ actions with respect to social and responsible behavior, sustainable business practices and ethics has shifted not only stakeholder but also company focus towards being in line with those requirements (Waddock et al., 2002). Nowadays, even historical and classical intrinsic capitalistic systems, like the capital market, seem to start acknowledging this tendency. Thus, Larry Fink, Chief Executive Officer (CEO) of the largest asset management firm in the world, Blackrock, announced in his annual letter in 2020 the need to address environmental issues (Blackrock, 2020). These examples only show some of the recent developments towards a society that appears to be more interested in corporations, which are actively participating in civil society.

This scientific and societal progress raises the question whether companies share this progressive idea and abide by it in practice. In order to answer this question, this paper employs the hypothesis that showing ethical as well as socially responsible activities might serve as proxy for the acknowledgement of being part of civil society.[1] In order to evaluate this awareness of social responsibility, firstly the terminologies „value“, ethics“ as well as „civil society“ need to be defined. Secondly, an exemplary company as subject to investigation needs to be determined. The selected company should ideally allow for easy access of information and be acting in an ethically challenging environment. After having selected Merck „Kommanditgesellschaft auf Aktien“ (KGaA)[2] as company for investigation, the company will be presented and ethically evaluated. For this, two ethical evaluation approaches are conducted. The two methodologies that can be seen as indicators of this recognition and engagement of social responsibility are the ethical corporation rating according to Hemel (2019b) as well as an investigation of the corporation’s business code in accordance with Kaptein (2004). Lastly, a conclusion with respect to the central question can be drawn and recommendations can be stated.

2 Values & Ethics in Civil Society

For the purpose of validating the hypothesis that companies define themselves as part of civil society, when they pursue societal values, the companies’ activities need to be evaluated. However, it is essential to establish an understanding for the predominant intersection between values and corporate activities beforehand. Also, some fundamental definitions need to be presented. As a result, this chapter will briefly represent definitions of related terminologies like „values“, „ethics“ and „civil society“ as well as clarify their intersection with corporate actions.

As economy is always part of a social and environmental structure, the persistent adherence of Friedman’s shareholder value principle that only considers humans as „homo oeconomicus“, can cause individual and societal damage (Joob, 2016, p. 100). This sense deficit of economic sciences and the related value conflict in civil society led to the actual discussion of corporate values towards civil society (Joob, 2016, p. 100). This illustrates that corporations are not detached from society, but rather act in the context of civil society (Beckmann, 2011, p. 8).[3]For these reasons corporate power should be followed by societal responsibility. By acknowledging and adhering individual and societal moral values, corporations can show the acceptance of their social responsibility. But how are value and ethics defined and which values should be followed?

According to Bechmann and Hartlik (2004, p. 31), values describe a „special relationship between valued objects and a valuing person. Namely, these objects are valuable to the person for some reason“. „An object (value carrier) is valuable to a valuing subject for satisfying some specific need (measure of value)“ (Joob, 2016, p. 105). This character of values serves as guidance measure of social action, as meaning giving and evaluation pattern for social reality (Dyllick and Probst, 1983, p. 30). Additionally, they „label ideal, desirable and pursuable things“ (Dyllick and Probst, 1983, p. 30). Even though values are partially relative and subjective, they are typically not arbitrary for they deal with physical and psychological human needs, which are determined by nature (Joob, 2016, pp. 108-109). Adherence to these values contributes towards human wellbeing and development (Joob, 2016, p. 110). Among others, human rights, trust, fairness, loyalty, honesty, responsibility, health, environmental quality and appreciation can be mentioned as examples of values (Joob, 2016, p. 111).

However, as there are typically many values involved in actions, two values can be substituting, indifferent, complementing and competing. Therefore, it is assigned to ethics, to consider the relationship between several values and preferably establish a value system that can serve as guidance measure for practice, without contradictions among these values. It is ethics that is commissioned with the critical exposure of these moral values and constitutes which values should be considered as publicly valid. (Joob, 2016, p. 112)

3 Company Selection & Ethical Challenges

In order to answer the question of companies practically acting towards socially desirable goals and understanding themselves as part of civil society, it can be hypothesized that this social behavior can be observed in the company’s activities. Therefore, an exemplary company will be determined. As it is necessary to be able to collect a vast amount of information about the company to evaluate it accurately, listed companies are of particular interest. „Deutscher Aktienindex 30“ (Dax 30) companies not only fulfill this criteria, but also include companies with a potentially high impact on society due to the company’s size. Additionally, these companies are usually also greatly interested in maximizing shareholder value. The sector of the company of investigation might be of interest, as well. With ethical challenges potentially perceived to be more delicate in some industries over others, the public might have higher ethical demands on some companies. Since Merck has been found to meet these criteria, it has been selected as exemplary subject of investigation for this study.

To evaluate the ethical position and responsibility of Merck, some of the company’s major potential ethical challenges need to be determined. As some of these ethical challenges represent crucial sanitary, economic, environmental and humane aspects of civil society, the respective company’s activities might constitute its acknowledgement of responsibility towards civil society. This serves the purpose of evaluating whether, firstly, Merck is aware of those challenges, and secondly, actively engaged in facing them in a socially desirable manner. In the following, some of the determined challenges will be specified:

Scarcity of drugs represents the need for drugs to not only be profitable for the company, but to safe- guard the essential supply of drugs at the same time.

Drug pricing describes Merck’s trade-off between profit maximizing for the shareholders and ethics that dictate affordable medical care.

Profitable manufacturing of qualitative drugs is concerned with pharmaceutical corporations being forced by high cost pressure of the competition to produce, for example, in non-European Union (EU) states. There they typically can manufacture drugs in a low-cost structure environment due to lower wages and regulatory restrictions. However, at the same time this might lead to challenges in ensuring high quality standards. For instance, supply chain impurities in products need to be averted.

Clinical tests represent another potential ethical challenge for Merck. As clinical tests are required for quality assurance and research, it is vital to conduct these tests. Nevertheless, some ethical standards need to be upheld, especially with respect to human and animal treatment procedure.

Study of rare but curable diseases describes the trade-off of the possibility to cure scarce diseases even though conducting research and development on respective drugs might not be profitable or otherwise de- sired by the company.

4 Company Overview of Merck

In order to examine whether Merck has acknowledged to be part of civil society, background information about Merck must be considered. Hence, this chapter will display not only general and financial information about Merck, but also its corporate code as well as corporate responsibility report. This information serves the purpose of providing background information for the ethical evaluation approaches following in chapters 5 and 6.

4.1 General & Financial Facts

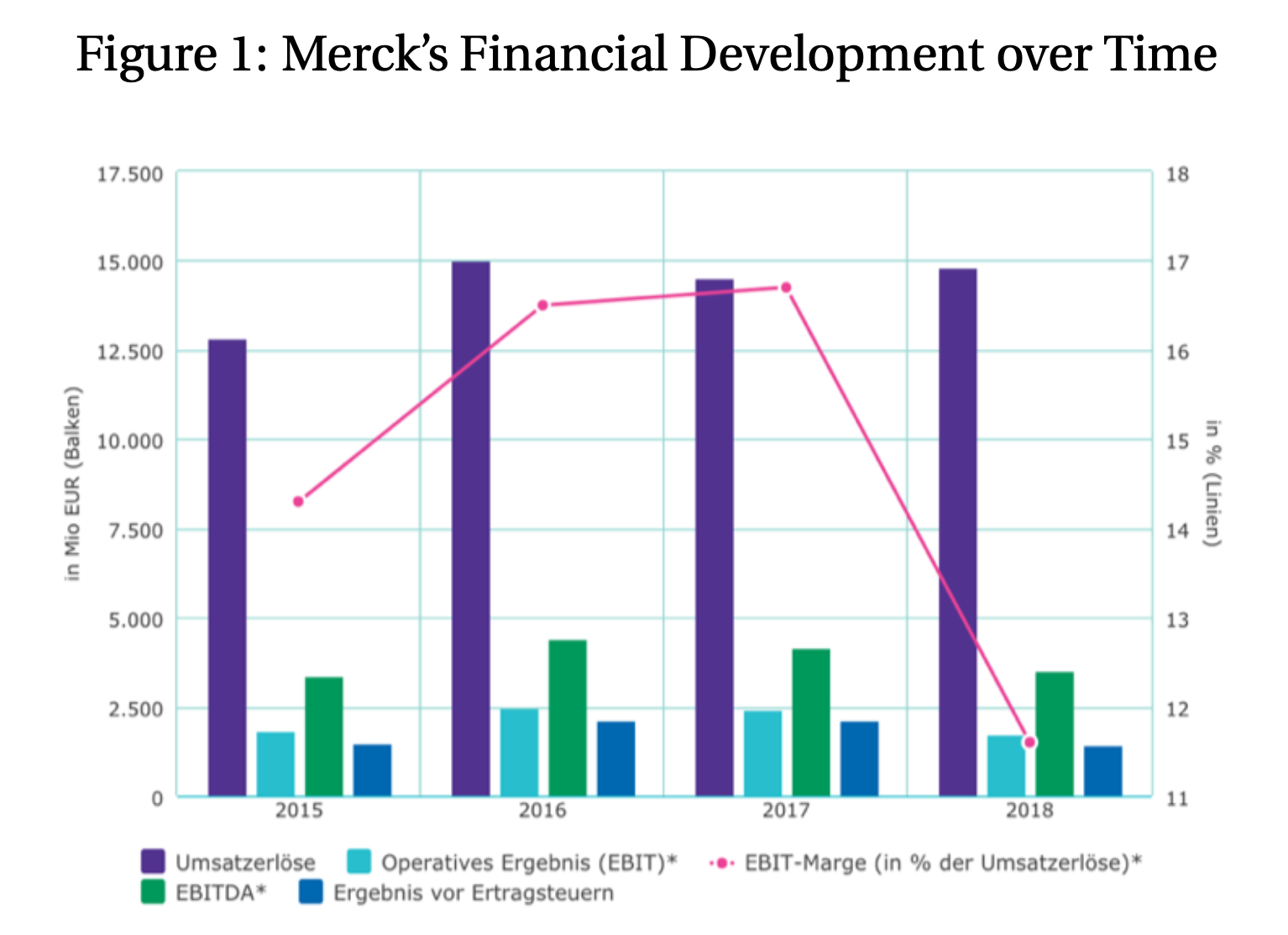

Merck, a chemical and pharmaceutical company founded in 1668 in Darmstadt (Germany), is represented in the most notable German stock index, called Dax 30. Merck’s ownership structure is still predominantly built by descendants of founder Friedrich Jakob Merck. With about 52,000 employees being represented in 66 countries, Merck focuses on healthcare, life-science and performance materials. While healthcare and lifescience both contribute 42% to the total company revenue, performance materials participates with 16%. The first business unit, healthcare, is composed of bio- and allergopharma, drugs as well as intelligent medical devices. Among others, the main concentrations of therapy within these areas range from allergies, fertility and neurodegenerative diseases to oncology. Secondly, the life-science division of Merck mainly focuses on the support for drug manufacturers especially in the areas of laboratory water systems, technology for genome editing, antibody and cell lineage, biotechnological systems as well as consumer safety for food and water. The third business unit, performance materials, is a specialty chemicals business. This division develops solutions for displays, computer chips and various kinds of surface materials. (Merck, 2019b)

According to Merck (2019a), the financial ratios especially in terms of revenue (14.8 billion (Bn)), result per share (7.76), share price (98.98) as well as Research & Development (R&D) (2.2 Bn) expenses improved compared with the previous year. However, the Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) (3.5 Bn) and Earnings Before Interest and Taxes (EBIT) (1.7 Bn) decreased by 15.3% and 28.7%, respectively.[4] This yearly development is shown in figure 1.

4.2 Corporate Code & CR Report

For the purpose of ethically evaluating Merck, which serves as proxy for the awareness and responsibility taken as part of civil society, not only the concrete undertakings, but statements of corporate responsibility need to be considered equally. As it is challenging to assess the company’s operational activities and respective intentions, the effort put in the code of conduct and corporate responsibility report might indicate awareness and acknowledgement for the determined challenges towards civil society. Thus, this subchapter will state and analyze Merck’s Corporate Code as well as their Corporate Responsibility (CR) Report. Additionally, it includes some publicly disseminated information on the company’s website.[5]

Merck’s Code of Conduct presents Merck as corporation that is aware of the link between corporate success and social as well as environmental consequences. Thus, Merck considers itself as „global corporate citizen which acts responsibly towards their employees, suppliers, business associates, customers as well as when dealing with nature and resources“ (Merck, 2017, p. 11). According to Merck (2017, p. 11), active engagement in initiatives and the public dissemination of Merck’s values can also be seen as a sign of commitment to these values and Merck’s social responsibility. However, this argument can be questioned, as this might not only be applicable for Merck, but for many, especially publicly listed companies.[6] of information dissemination might not only be intrinsically, but extrinsically motivated.

The code of conduct states some main corporate values that should guide and govern all corporate actions. According to Merck (2017, p. 13), these values are integrity, achievement, respect, responsibility, transparency as well as courage. While achievement is seen as precondition to enable entrepreneurial independence, courage means to also follow ideas that might seem unconventional and challenge the status quo, integrity, respect, responsibility and transparency on the other hand, are concerned with credibility by following the corporate values in all transactions and building the corporate actions on a respectful, responsible and transparent foundation involving all stakeholders as well as natural resources (Merck, 2017, pp. 14-35). Additionally, these values are subdivided into the following, more concrete areas: UN Global Compact 2005, principles in the workplace, principles for dealing with external business partners and customers and principles on social responsibility (Merck, 2017, pp. 14-35). The code also includes human rights, working standards, environmental protection and anti-corruption guidelines as part of the UN Global Compact Goals, signed by Merck in 2005 (Merck, 2017, pp. 14-35). Among others, the principles in the workplace cover topics like trustful collaboration, diversity, dignity and privacy of the individual (Merck, 2017, pp. 18-23). Most aspects are formulated extremely detailed and supported by examples. For instance, it is stated that discrimination due to gender, ethnic origin, religion, disabilities, age and sexual orientation is not tolerated (Merck, 2017, p. 19). Furthermore, the principles for dealing with external partners and customers cover the cooperation with authorities, fair competition, clinical study ethics as well as fair and transparent selection of suppliers (Merck, 2017, pp. 24-29). Further examples are the principles on social responsibility which covers the realms of product safety, ethical responsibility and retention of natural resources (Merck, 2017, pp. 30-35). Merck even precisely states to „be part of society“ (Merck, 2017, p. 31). Moreover, some major compliance topics, contacts and procedures are stated and discussed at the end of the code.

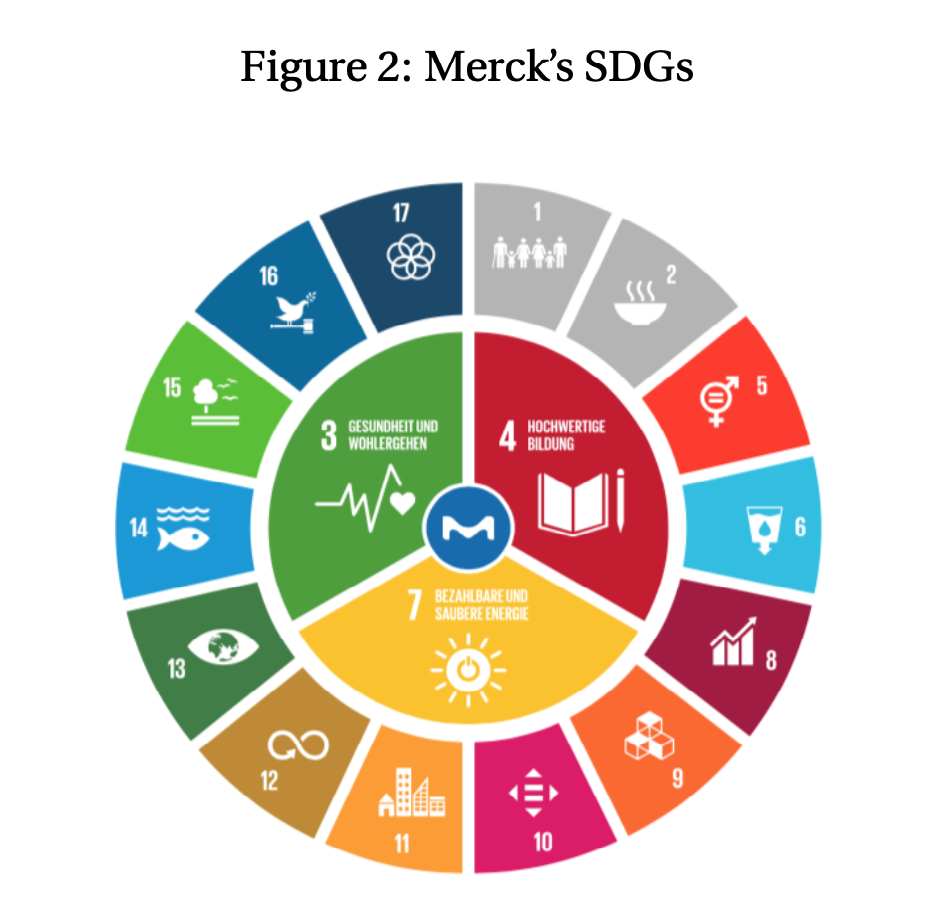

Another source that has been considered as evidence for the awareness of responsibility is Merck’s corporate responsibility report (Merck, 2019a). This report consists of the SDGs, examples of company activities towards these goals, the corporate strategy as well as corporate responsibility strategy and target tracking tools. With respect to the SDGs, Merck focuses mainly on Health and Welfare, High-quality Education and Affordable and Clean Energy (Merck, 2019a, p. 176). Furthermore, four SDGs are contributed to in a „significant scope“, while eight more are contributed to in a „small scope“ (Merck, 2019a, p. 176). Thus, according to this report, only the goals relating to No Poverty and No Hunger are not considered by Merck’s corporate actions. A visual representation of this weights of Merck’s contribution to the SDGs can be seen in figure 2.

In addition to stating the abstract contribution towards those goals, the corporate responsibility report also depicts exemplary projects that contribute to the respective goals (Merck, 2019a, pp. 159-172). Among others, they state concrete actions against bilharzosis, which contributes to Sustainable Development Goal 3 (SDG3) (Merck, 2019a, p. 65). Moreover, the 15 SDGs are further supported by more precise subtargets of the respective goals (Merck, 2019a, pp. 177-180). The measures, progress, timeline as well as status of the respective subtarget is also stated and traceable on the company’s website.[7] These subtargets and tracking tools are also divided into topic groups such as business ethics, products, employees and environmental protection (Merck, 2019a, pp. 19-129). Additionally, Merck’s corporate strategy is defined as responsible actions with respect to employees, products, environment and society (Merck, 2019a, pp. 8-10). With respect to the formerly identified potential ethical challenges in chapter 3, it can also be noted that Merck’s corporate responsibility report addresses each and every one of those in detail.

5 Ethical Evaluation Methodologies

To evaluate Merck’s awareness of being member of civil society, this chapter will focus on two methodologies.[8]While the ethical corporation rating according to Ulrich Hemel aims at evaluating the corporation through participants’ perception of corporation activities, an evaluation of corporate code in accordance with Muel Kaptein is based on a comparison and analysis of a corporation’s code. This chapter briefly represents these methodological approaches.

5.1 Ethical Corporation Rating according to Ulrich Hemel

The ethical corporation rating according to Ulrich Hemel is based on two main ideas. The consideration and examination of facts as well as actions by the corporation and the respective perception of the corporation’s undertakings by the public. According to this methodology, the perception of a corporation’s ethical behavior will be determined at two points in time: before and after a more precise study of the corporation.[9] The underlying idea is to quantify the perceived company’s behavior by the participants with only common knowledge before, and with more extensive knowledge after the study. The questions to be answered remain constant over time.[10] The survey consists of ten equally weighted questions, capturing the perception of the corporation of interest. The covered topics represent a wide range of socially and ethically relevant aspects. Among others, these are concerned with the transparency of information, responsibility for SDGs, quality of governance as well as public credibility. Every topic can be evaluated on a ten-point scale. The scale ranges from 0 to 10, with 10 representing the highest and most positive score. The average value of the ten single scores results in a total score. Figure 3 depicts all aspects of the ethical corporation rating and potential answers of an exemplary ethical corporate evaluation with pre- and post-study results. (Hemel, 2019b)

For the overall assessment, many aspects influence the perception of the corporation’s behavior and should be considered. Among others, company facts, ethical challenges, structures of responsibility, including governance, as well as recommendations for how to improve the ethical and social perception can be taken into consideration. As depicted in figure 3, the entirety of qualitative information will then be summarized and quantified through the ethical evaluation rating. The average score before and after the study can not only be interpreted independently, but compared over time. This allows for additional information insights about the participants’ perception of the company’s activities.

5.2 Evaluation of Corporate Codes according to Muel Kaptein

The study „Business Codes of Multinational Firms: What do they say?“ by Kaptein (2004), investigated the corporate codes of the 200 largest corporations in the world. It was the aim of this study to examine if and to which extent corporations are aware and concerned with interests of their stakeholders and core values, especially with respect to ethics, sustainability as well as social responsibility (Kaptein, 2004). Some of the aspects that have been analyzed range from transparency, adherence to laws, environmental protection to corruption (Kaptein, 2004). The methodology as well as the results of this study will be briefly presented in this chapter.

Using the SCOPE Core Company list by Van Tulder et al. (2001), Kaptein (2004) contacted the respective company headquarters and requested their business codes. For this purpose, business codes have been defined as „independent, company-specific policy document which delineates company responsibilities towards stakeholders and/or employee responsibilities“ (Kaptein, 2004, p. 13). After having received the respective codes, the content was classified into various topics in accordance with the corporate integrity model developed by Kaptein, Wempe, et al. (2002). Intention of this model was to differentiate between „company responsibilities towards stakeholders, principles governing stakeholder relationships, corporate values and employee responsibilities towards the company“ (Kaptein, 2004, p. 17).

While the contents of the business codes were examined with respect to several criteria, such as „prevalence, title, content and size“, also recommendations for improvement were derived and presented (Kaptein, 2004, pp. 17, 27). The cross-country analysis demonstrates, that most of the 200 largest companies (52.5%) proved to possess corporate codes, with United States (US) companies being represented dominantly (Kaptein, 2004, p. 17). With respect to the titles used, it could be shown that there was a great deviation between the companies (Kaptein, 2004, p. 17). Moreover, the business codes’ contents were analyzed with respect to stakeholder responsibilities, stakeholder principles, corporate values as well as implementation and compliance. Kaptein (2004, p. 21) found that transparency, honesty and fairness are the most frequently incorporated stakeholder principles within the investigated business codes. Again, descriptive differences by country and continent could be found (Kaptein, 2004, p. 21). With respect to the corporate values it could be demonstrated that teamwork and responsibility were cited the most important by the companies under investigation (Kaptein, 2004, p. 22). However, as argued by Kaptein (2004), content is only one aspect that can be subject to assessment. Another potential subject is the demonstration of a corporation’s awareness of socially relevant topics as well as the implementation of them in practice (Kaptein, 2004, p. 17). Kaptein (2004, p. 27) therefore states some general suggestions for quality codes, which have been derived from this study. According to those suggestions, company codes should be concerned with Accountability, Feedback, Stimulating Work Environment, Periodic Update, Clear Status, Availability, Convincing Message, Clear Structure, Appropriate Presentation and a Unique Identity. While Kaptein (2004) represents many potential aspects that could be taken into account when analyzing a business code as proxy for the awareness and responsibility that a company takes as part of the civil society[11] it was decided to follow these summarizing recommendations as reference for this assessment. This helped to overcome constraints in time and scope as well as practical challenges when comparing the entirety of study findings with Merck’s code of conduct.[12]

However, when considering the results of Kaptein (2004), it should be taken into account that this study might be limited in its external validity, as there might be a reason to why some companies did not respond to the request of disseminating their business codes (Kaptein, 2004, p. 17). Thus, it is possible, that companies fearing to have a weak corporate code did not submit it, resulting in a selection bias of the study. Additionally, with respect to the commitment of the corporations, it might still remain unclear why companies pursued a specific action in their business code. This might be due to ethical or economical reasons (Kaptein, 2004, p. 17).

6 Results

After having stated fundamental background information as well as having identified some major ethical challenges in chapters 2 to 4, evaluations in accordance with the presented methodologies have been con- ducted. Following these approaches, this chapter will focus on displaying the respective results as well as stating some final pieces of advice with respect to improving Merck’s company activities and structures.

6.1 Results – Ethical Corporation Rating

In accordance with the ethical corporation rating presented in chapter 5.1, a panel survey has been conducted at two different points in time. The first survey was undertaken in the beginning of the lecture about Merck’s corporate activities, on January 8th 2020. The participants in the survey were graduate business students with various majors, but participating in the same business ethics class. In order to establish a reference value, the questionnaire has been answered by students, who did not extensively study the company. Thus, a comparison between the evaluation of these students (Class Rating) and my own assessment (My Rating) was conducted. The results of the pre-study evaluation of Merck can be seen in table 1. Table 1 not only states the criteria, but single scores, total scores as well as average scores (Avg.) for my own and the class evaluation. It can be seen, that the overall rating between both groups shows a close similarity with total average scores of 4.50 and 4.60. Moreover, it is noteworthy that Employer’s Attractivity reaches the highest score at 7 and 8 for both ratings. This result suggests that, despite Merck’s Employer’s Attractivity, little information about Merck’s activities is outstanding for the uneducated participants.[13]

After having established the uneducated baseline reference in the pre-study condition, the participants have been lectured about Merck. Among others, sources included general and financial facts as well as Merck’s code of conduct and corporate responsibility report. Afterwards, the same survey with respect to the ten ethical criteria has been performed again. Table 2 represents the results of this post-study evaluation. When looking at table 2, it can be noted that both My Rating as well as the Class Rating show a bigger deviation between each other than before.[14] Nevertheless, the absolute difference of 1.20 might not lead to the conclusion of very divergent perceptions about Merck. Again, Employer’s Attractivity scores the highest in both assessments. When comparing the results of the pre-study and post-study ratings in more detail, table 3 shows an overall improvement of the average rating by 2.75 points. This equals a 60% increase as compared to the initial pre-study total score. In addition, every single criterion shows an absolute and hence also relative increase. The result suggests, that gaining more information about Merck’s corporate activities improves the participants’ perception of Merck acting socially and ethically over all criteria.[15] Some strongly increased individual topics are the Transparency of Information and the Ethical Ability to take Criticism, with improvements in evaluation of 143% and 167%, respectively. As opposed to this, the Quality of Communication“ as well as the Employer’s Attractivity remained relatively constant with small improvements of 10% and 20%.

In general, however, it should also be mentioned that the number of observations being included in this study was extremely small. Thus, only three students participated in the Class Rating. Moreover, it should be considered, that this study might be biased in selection, as this study was only conducted within a specific business ethics class, limiting the external validity of the study. Conducting tests of differences for the total

average scores across groups as well as over time might also add further value to this study for it could indicate whether the results deviated not only economically but statistically significant.[16]

6.2 Results – Evaluation of Corporate Code

After having analyzed Merck’s code of conduct with respect to the recommendations described in chapter 5.2, it can be found that most of the ten criteria have been assessed as fulfilled. Table 4 depicts the summa- rized and commented assessment of all recommendation criteria by Kaptein (2004). It shows that only two criteria are insufficiently included, namely Periodic Update as well as Unique Identity. This was especially due to missing explicit statements covering the regular updates of the code and generic statements about Merck, that were found to be imprecise. Moreover, no annual Accountability in terms of implementation and compliance was addressed by Merck’s code of conduct. However, this topic was at least addressed in the corporate responsibility report (Merck, 2019a, p. 21). The Clear Status of the Code was found to be another topic for improvement. Merck’s code of conduct only implicitly communicates the perception of being a guideline for behavior, rather than explicitly stating to be a concrete and mandatory policy. Yet, the code mentions that it is supported by „mandatory policies“ for „specific topics“ of the company (Merck, 2017, p. 12). All other recommendation criteria by Kaptein (2004) have been found to be fulfilled. Exemplary, the Feedback criterion was well captured in Merck’s code of conduct. Merck’s business code explicitly invited internal as well as third party stakeholders to contribute in feedback when points of improvement have been identified (Merck, 2017, pp. 38-39). This was only stated by 5% of the examined codes by Kaptein (2004). Moreover, Merck’s code of conduct stated information about the compliance reporting process, including responsible contact persons and a phone number to contact (Merck, 2017, pp. 38-39).[17] Additionally, the availability and easy access of the code should be highlighted. While Kaptein (2004, p. 28) reports that obtaining the examined business codes was „cumbersome“, Merck’s code of conduct and every other information related to this code or the corporate responsibility report was easy to find and highly transparent.

Overall, it can be stated that six of the criteria could be found to be fully and sufficiently addressed.[18] Two more criteria only have been assessed as partially fulfilled. This leads to an overall rate of sufficiently accomplished code recommendations of more than 60%. Therefore, it can be stated that Merck’s code of conduct meets most of the recommendations made by Kaptein (2004). This result indicates that Merck is highly committed to promote compliant and transparent behavior not only within the company, but also with respect to the public. Again, according to the previously constructed hypothesis, this might be seen as evidence of Merck’s acknowledgement of responsibility towards civil society.

7 Conclusion

Having studied and analyzed Merck’s corporate information, the code of conduct as well as the corporate responsibility report, it can be noted that Merck seems to be aware of their ethical and social affiliation to civil society. This inference is due to the fact that Merck seems to be aware of the interaction between corporate culture, corporate values and corporate strategy. They clearly define their corporate values in a detailed manner, while at the same time pursuing activities that enable a matching corporate culture.[19] Moreover, they appear to incorporate these values and culture into their overall corporate strategy. This acknowledgement of interdependencies builds the basis for an ethical and social long-term orientation of Merck.

Additionally, the two ethical evaluation methodologies further support this perceived awareness and pursuit for ethical, social and sustainable responsibility. While studying Merck’s corporate information increased the average perception of Merck’s ethical and social behavior by 60% on the ten-point scale, it suggested that Merck contributes more to civil society than initially expected. Furthermore, the code of conduct accomplished most of the recommendations made by Kaptein (2004), hence indicating to be a detailed, elaborate and well structured business code. This proved effort further supports the overall perception of Merck’s awareness of responsibility and contribution towards civil society. As mentioned in chapter 4.2, Merck even states to „be part of society“ (Merck, 2017, p. 31).

Even though the results from my analysis show that Merck seems to be doing well with respect to ethical behavior, it is important to highlight that these were only two very brief evaluation methods. For that reason, other approaches might be interesting to conduct in order to verify the results.[20] It should also be taken into account that this paper’s ethical evaluation with respect to Kaptein (2004) is based on a study that was conducted in 2004. As this study is about 16 years old, there might have been some development in business codes in general. It might therefore be valuable, to undertake another similar comparison with a more recent study of peer company’s business codes.

Moreover, the negligible number of observations with similar professional backgrounds, building the basis for the ethical corporation rating according to Hemel (2019b), should be addressed in future studies. Thus, a more extensive study should be conducted, controlling for different individual characteristics and potential country factors. The higher number of observations as well as less selectively chosen participants might increase the external validity and hence the generalizability of this study. A broadly conducted panel data survey with a fact study period in between might be appropriate for this approach. This approach might capture the perception of citizens about Merck’s activities more accurately.

One last aspect of improvement of this study might be concerned with the study period. Thus, it might be meaningful to not only allow for a single student educating the remaining participants. As the analysis of corporate depiction through corporate codes and responsibility reports is a matter of subjectivity, the education process might be biased. In order to not influence the perception of the educated participants, a better scenario might include self-education about the company. This way, the „mental architecture“ of the teaching individual does not infiltrate the other perceptions (Hemel, 2019a, p. 335).

Following this study, with Merck being an exemplary representative of large companies and their attitude towards civil society, we can conclude that at least some companies seem to be aware of their position as part of civil society. However, we can of course not generalize this to all corporations (large or small). It should also be mentioned, that the fact that Merck still is a family owned company might contribute to this result. Additional to the limitations mentioned above, a far more extensive study with several companies from various industries, sizes and countries should be analyzed. As consequence of these limitations, there is the need to conduct further research.

8 Conclusive Recommendations for Merck

After having studied and analyzed Merck’s general information, their corporate responsibility report and their code of conduct, two recommendations can be given in order to improve Merck’s perception in public.

Firstly, the introduction of a new board of director position might be valuable. Appointing an expert as member for compliance and responsibility to the board of directors might increase the perception of ethical issues being concerned about and addressed by the management. In addition to the typical positions being represented in the board of directors, such as CEOs for the various business units, one central Chief Financial Officer (CFO) as well as the chairman of the board, this might underline the company’s ethical responsibility towards the public.

Secondly, the public communication of Merck’s ethical efforts should be focused on. It seems to be the case that Merck quite actively is not only considering ethical aspects, but actively engaging in those. This effort should be communicated to the public appropriately. Here, however, one should be aware of finding an appropriate blend between the scope as well as the method to communicate this to the stakeholders. As mentioned by Kaptein (2004, p. 29), the representation of the ethical behavior is of considerable importance. Some efforts might otherwise be perceived as pure marketing instruments rather than actually communicating and encouraging ethical as well as social spirit.

References

Bechmann, Arnim and Joachim Hartlik (2004). Die Bewertung zur Umweltverträglichkeitsprüfung-ein methodischer Leitfaden: Grundlagen, Konzept, Arbeitsmodelle, Vorgehensweise. Edition Zukunft.

Beckmann, Markus et al. (2011). Was ist corporate social responsibility (CSR)? RHI – Discussion, Nr. 17.

Blackrock (2020). A Fundamental Reshaping of Finance. URL: https://www.blackrock.com/corporate/ investor-relations/larry-fink-ceo-letter (visited on 02/14/2020).

Carroll, Archie B et al. (1991). “The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders”. In: Business horizons 34.4, pp. 39–48.

Dyllick, Thomas and Gilbert JB Probst (1983). “Lebensgrundlagen und Werthaltungen im Wandel”. In: Mitarbeiterführung und gesellschaftlicher Wandel, Bern-Stuttgart, pp. 17–48.

Freeman, R Edward (2001). “A stakeholder theory of the modern corporation”. In: Perspectives in Business Ethics Sie 3, p. 144.

Friedman, Milton (1970). “The social responsibility of business is to increase its profits”. In: New York Times Magazine.

Hemel, Ulrich (2019a). “Mentale Architekture und Wirtschaftsanthropologie – eine Zukunftsaufgabe”. In: Anthropologie und Spiritualität für das 21. Jahrhundert. Ed. by Sebastian Kießig and Marco Kühnlein. Vol. 80. Verlag Friedrich Pustet, pp. 335–350.

— (2019b). Werteorientierung und Vertrauensbildung-Welche Art des Wirtschaftens hilft? Weltethos-Institut.

Joob, Mark (2016). “Ethische Werteorientierung in Unternehmen”. In: Ethica – Wissenschaft und Verantwortung Jg. 24 Nr. 2, pp. 99–117.

Kaptein, Muel (2004). “Business codes of multinational firms: what do they say?” In: Journal of Business Ethics 50.1, pp. 13–31.

Kaptein, Muel, Johan Ferdinand Dietrich Bernardus Wempe, et al. (2002). The balanced company: A theory of corporate integrity. Oxford University Press, USA.

Merck (2017). The Merck Code of Conduct. URL: https://www.merckgroup.com/id/compliance/English_Merck_CoC_new.pdf (visited on 02/10/2020).

— (2019a). Corporate Responsibility Bericht 2018. URL:https://www.merckgroup.com/de/cr-bericht/ 2018/serviceseiten/downloads/files/gesamt_merck_crb18.pdf (visited on 03/16/2020).

— (2019b). Merck – Who we are. URL: https://www.merckgroup.com/company/de/WhoWeAre_DE.pdf (visited on 03/12/2020).

Porter, Michael E and Mark R Kramer (2011). “Creating Shared Value”. In: Harvard Business Review 89, p. 62.

Sachs, Jeffrey D (2012). “From millennium development goals to sustainable development goals”. In: The Lancet 379.9832, pp. 2206–2211.

Van Tulder, Rob, Douglas Van Den Berghe, and Allan Muller (2001). “The world’s largest firms and internationalization”. In: Rotterdam: Rotterdam School of Management.

Waddock, Sandra A, Charles Bodwell, and Samuel B Graves (2002). “Responsibility: The new business imperative”. In: Academy of Management Perspectives 16.2, pp. 132–148.

Glossary

| Avg. | Average |

| Bn | Billion |

| CEO | Chief Executive Officer |

| CFO | Chief Financial Officer |

| CR | Corporate Responsibility |

| Dax 30 | Deutscher Aktienindex 30 |

| EBIT | Earnings Before Interest and Taxes |

| EBITDA | Earnings Before Interest, Taxes, Depreciation and Amortization |

| EU | European Union |

| GAAP | Generally Accepted Accounting Principle |

| KGaA | Kommanditgesellschaft auf Aktien |

| N | Sample Size |

| R&D | Research and Development |

| SDG | Sustainable Development Goals |

| SDG3 | Sustainable Development Goal 3, „Health and Welfare“ |

| UN | United Nations |

| US | United States |

Appendix

[1] Since this assumption is solely based on a potential logical causality between the acknowledgement of the affiliation to a group (here civil society) and the respective ethical behavior, this hypothesis might be needed to be validated in further studies.

[2] In order to ensure readability Merck KGaA will be abbreviated as Merck for the rest of this paper.

[3] Here, civil society is understood as „all forms of non-governmental actions“ according to Ulrich Hemel in (Beckmann, 2011, p. 8). Agents of civil society are not only natural persons, but comprehensive organizations like associations, non-governmental organiza- tions and corporations (Beckmann, 2011, p. 8).

[4] With respect to interpretability of this financial data, it might be valuable to consider this data in relation to peer companies. Due to restrictions in scope and time of this paper this comparison has been discarded.

[5] „https://www.merckgroup.com/de/cr-bericht/2018/„

[6] Thus, the public dissemination of financial information might not only be voluntarily, but required, as Merck is, among others, subject to compliance with Generally Accepted Accounting Principles (GAAPs). Moreover, non-disclosure of additional data, such as sustainability and responsibility related information, might be seen as competitive disadvantage in relation to peers and therefore economically harmful.

[7] „https://www.merckgroup.com/de/cr-bericht/2018/„

[8] Also, independent external research about potential scandals has been conducted to validate the actively and publicly disseminated information by Merck. However, as the number of scandals was extremely small in comparison to peers, this was perceived to be a positive indicator for Merck’s social awareness. Nevertheless, this information was considered in the performed education process and is therefore included in this study result.

[9] In the following chapters of this paper, the terminology used to address those two points in time will be „pre- and post-study period“.

[10] Thus, this data can be seen as panel data survey.

[11] Possible topics for assessment could have been the general prevalence, size and contet of a code as compared to Merck’s code of conduct. This could have been further separated and analyzed not only in general, but by country or continent.

[12] The large scope of Kaptein (2004) would have made it necessary to focus only on certain topics, while neglecting others. Following the summarized and derived recommendations made it feasible to achieve an overall assessment of the corporate code in question.

[13] Here, being uneducated is defined as the pre-study condition with respect to Merck assubject of study.

[14] While the pre-study deviation between the two ratings amounted to 0.1, the post-study survey showed an increased difference of 1.2.

[15] However, it should be considered the influence of a potentially subjective lecture, based on the lecturer’s individual „mental architecture“ (Hemel, 2019a, p. 335). According to Hemel (2019a, p. 335), „mental architecture“ describes the entirety of individual „experience, moods and dispositions“ that shapes a persons viewpoints. Therefore, other lecturers might have led to diverging results.

[16] Due to time constraints and the limited sample size (N=3) this additional procedure was found to be statistically not meaningfull in terms of added information and therefore discarded for this study. However, with increased sample size it should be considered.

[17] For more detailed information it refers to Merck’s intranet.

[18] However, it should also be taken into account that this is a subjective evaluation, as there is no clear rule as to when are commendation can be considered accomplished.

[19] Merck’s code of conduct stated the pursuit of hiring and retaining employees with a matching social and ethical attitude.

[20] As means of robustness checks, further as well as more detailed studies could be conducted. Among others, a detailed comparison study between the results found by Kaptein (2004) and Merck’s corporate code could be undertaken as mentioned in chapter 5. Moreover, comparisons could consider country, continent and industry differences.

Alle Rechte vorbehalten.

Abdruck oder vergleichbare Verwendung von Arbeiten des Instituts für Sozialstrategie ist auch in Auszügen nur mit vorheriger schriftlicher Genehmigung gestattet.

Publikationen des IfS unterliegen einem Begutachtungsverfahren durch Fachkolleginnen- und kollegen und durch die Institutsleitung. Sie geben ausschließlich die persönliche Auffassung der Autorinnen und Autoren wieder.